Short selling against US life insurance companies is rising sharply, driven by investor fears that insurers’ growing exposure to private credit carries hidden risks. Over the past decade, insurers have doubled their private credit holdings, a less transparent lending market where stress can surface abruptly. The result: more aggressive bearish positions as confidence in underwriting and credit resilience gets tested.

India’s life insurance sector has crossed $1 trillion in assets under management, driven by rising savings and a fast digital shift in how people buy policies. Supportive regulation, better technology, and changing customer behavior are moving purchases online, expanding choice and tightening pricing. As protection merges with savings, life cover is becoming a mainstream financial tool.

Your news, in seconds

Get the Beige app — every story in 60 words, updated hourly. Free on iOS & Android.

The EPFO EDLI Scheme provides lump sum death benefits for private sector salaried employees, typically between Rs 2.5 lakh and Rs 7.5 lakh. Recent changes also guarantee a minimum payout of Rs 50,000 for early deaths and factor in service continuity gaps, shaping eligibility for families seeking the claim amount.

India’s life insurance industry saw new business premiums rise 16% to ₹4.59 lakh crore in FY26. Analysts attribute the jump to GST relief benefits, increased demand for regular premium policies, and a deliberate tilt toward higher-margin protection and long-term savings products. The shift signals insurers are optimizing both growth and profitability as customer preferences evolve.

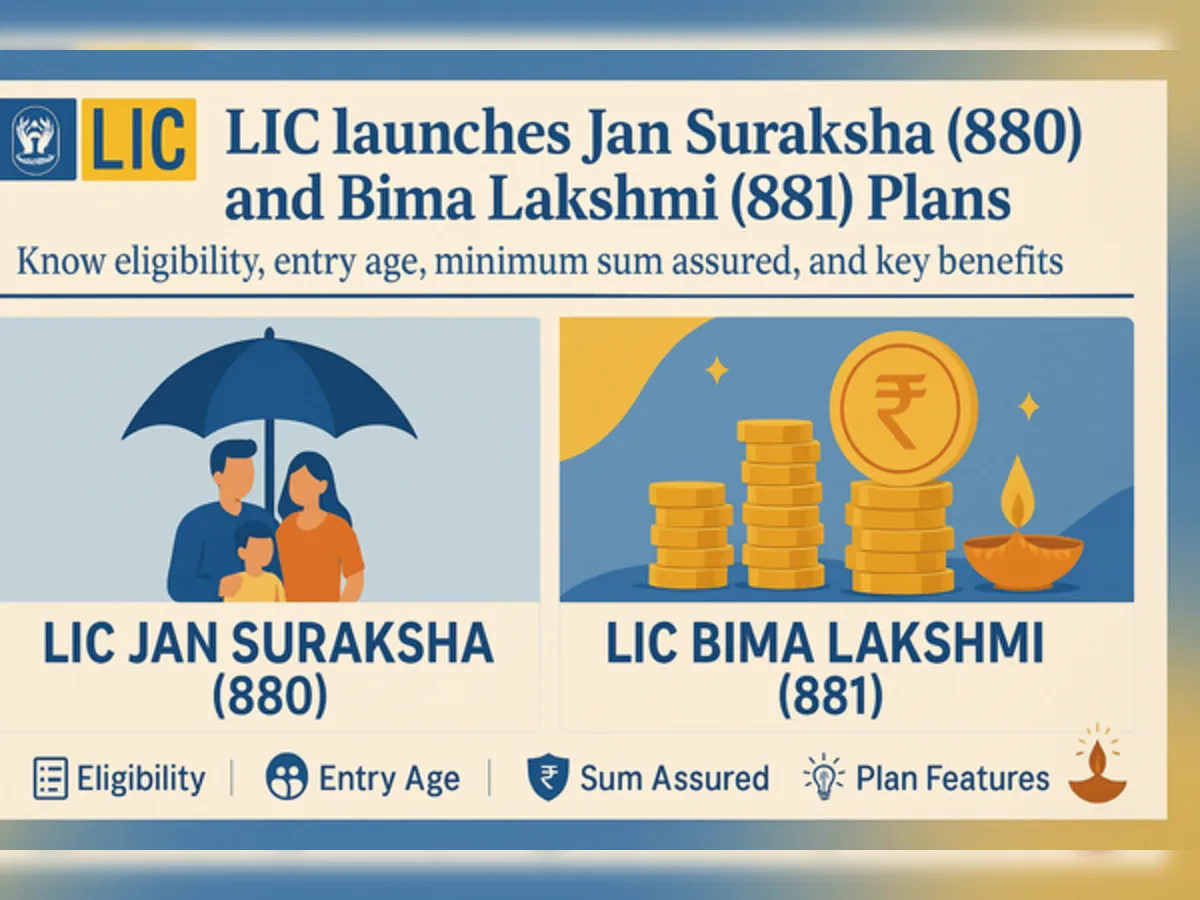

LIC has unveiled two new life insurance products: Jan Suraksha 880 for lower-income customers and Bima Lakshmi 881 exclusively for women. Both offer life cover, while Bima Lakshmi adds periodic money-back options and critical illness coverage. The launches mark LIC’s first products released under the new GST regime, bringing fresh eligibility terms and benefits to customers.

Swipe through stories, personalise your feed, and save articles for later — all on the app.